This work addresses device activity detection in massive machine-type communications (mMTC) for IoT.

Traditional methods assume Gaussian noise, which fails under heavy-tailed or impulsive noise. The toolbox contains source codes for the proposed algorithms,

RCWO (Robust Coordinate-Wise Optimization) and RCL-MP (Robust Covariance Learning-based Matching Pursuit), that use robust loss functions to improve detection in non-Gaussian noise environments. Simulation examples are also provided.

For more information, see: Robust activity detection in massive random access, IEEE Transactions on Signal Processing, vol. 73, pp. 3513-3527, 2025.

[ Github]

Github]

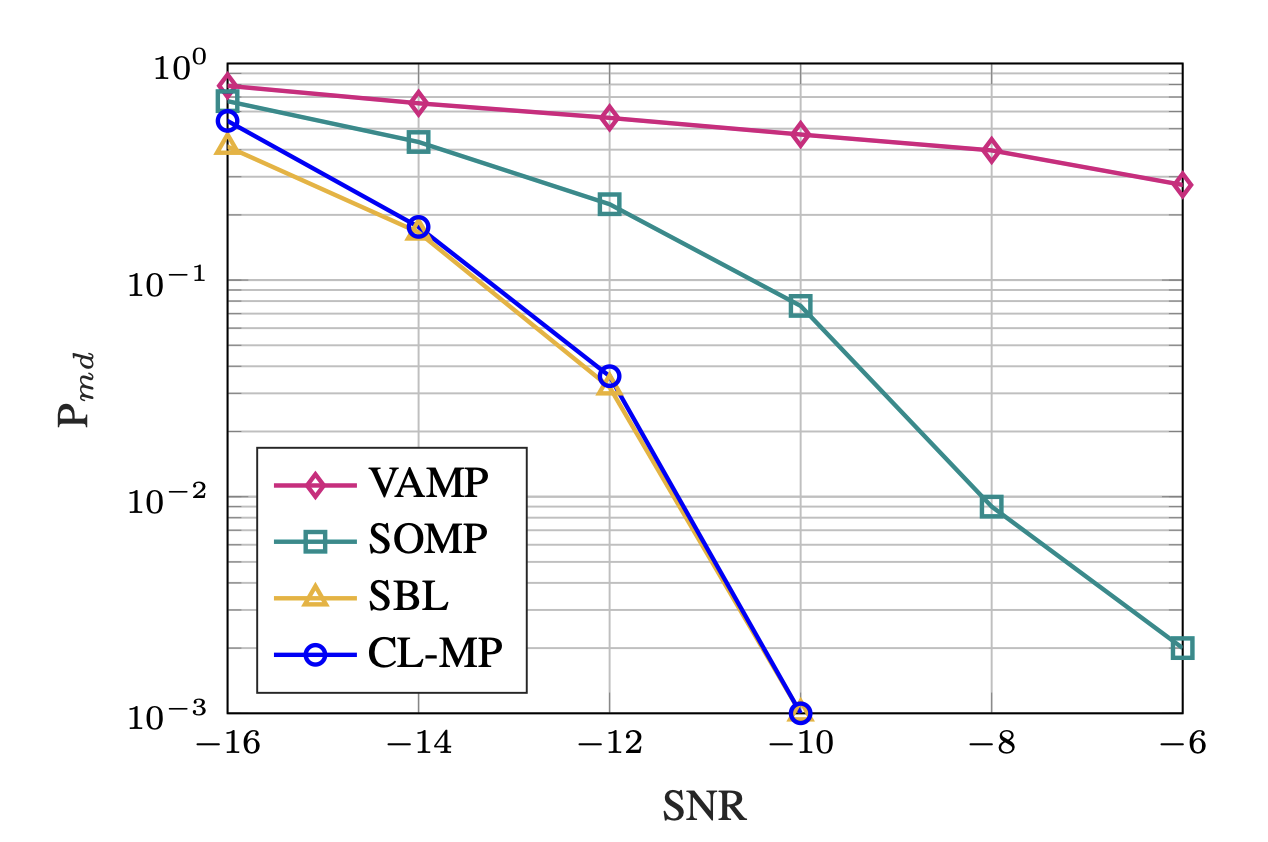

Activity detection using Covariance Learning Matching Pursuit

Activity Detection for Massive Random Access using Covariance Learning Matching Pursuit (CL-MP) method.

Also a demo simulation in the paper is provided.

For more information, see:

Activity Detection for Massive Random Access using Covariance-based Matching Pursuit, Leatile Marata, Esa Ollila, Hirley Alves, arXiv:2405.02741 [eess.SP]

For more information, see:

Activity Detection for Massive Random Access using Covariance-based Matching Pursuit, Leatile Marata, Esa Ollila, Hirley Alves, arXiv:2405.02741 [eess.SP]

[Github]

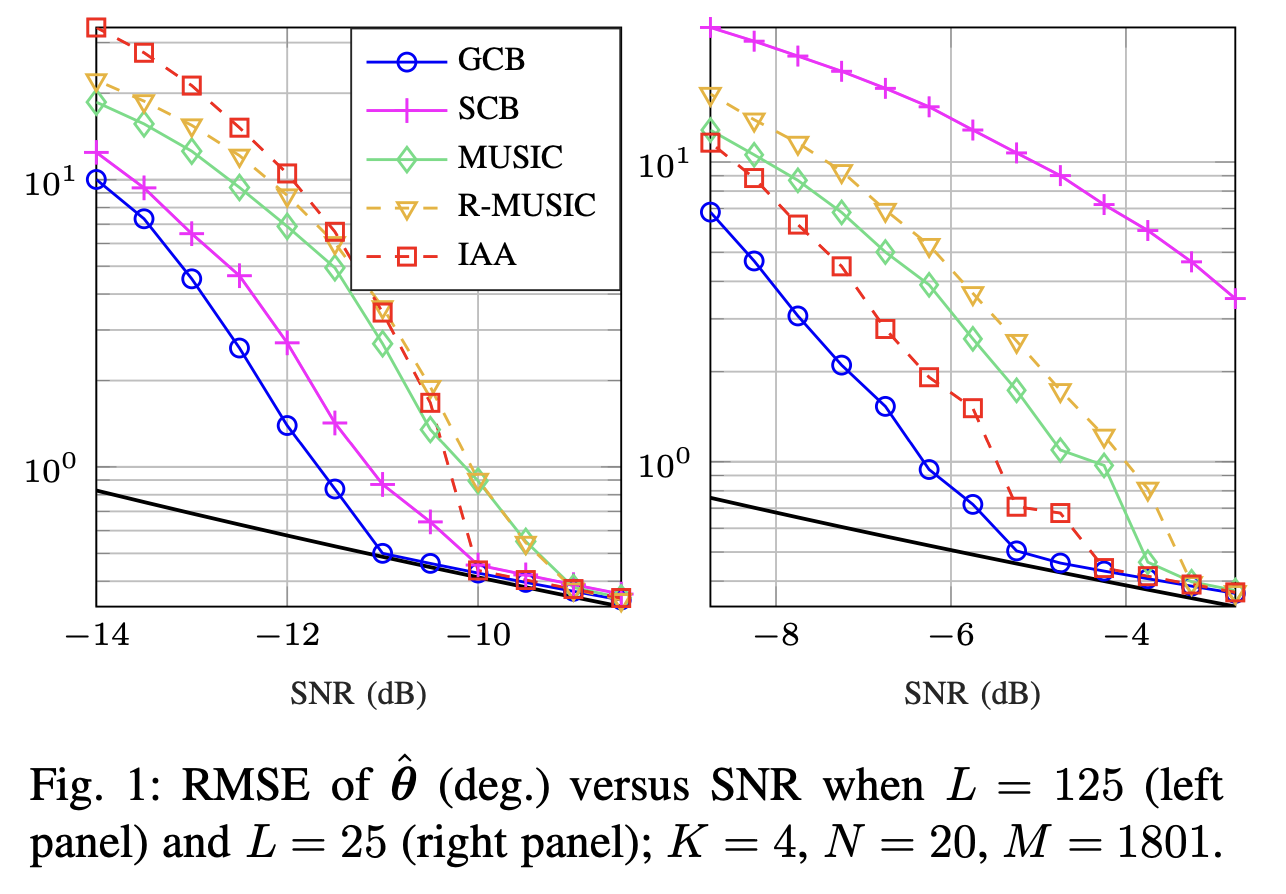

Greedy Capon Beamformer

We provide an efficient function to compute the Greedy Capon Beamformer (GCB) which is a (sparse) greedy version of the standard Capon Beamformer (SCB). GCB is fast to compute, often outperforms SCB with a clear margin,

and unlike the SCB it is not affected by coherence of the signals. In the Github repo, we also include a demo example that can be used to reproduces Figures

in the paper.

For more information, see:

Greedy Capon Beamformer, Esa Ollila arXiv:2404.15329 [eess.SP], Apr. 7, 2024.

For more information, see:

Greedy Capon Beamformer, Esa Ollila arXiv:2404.15329 [eess.SP], Apr. 7, 2024.

[Github]

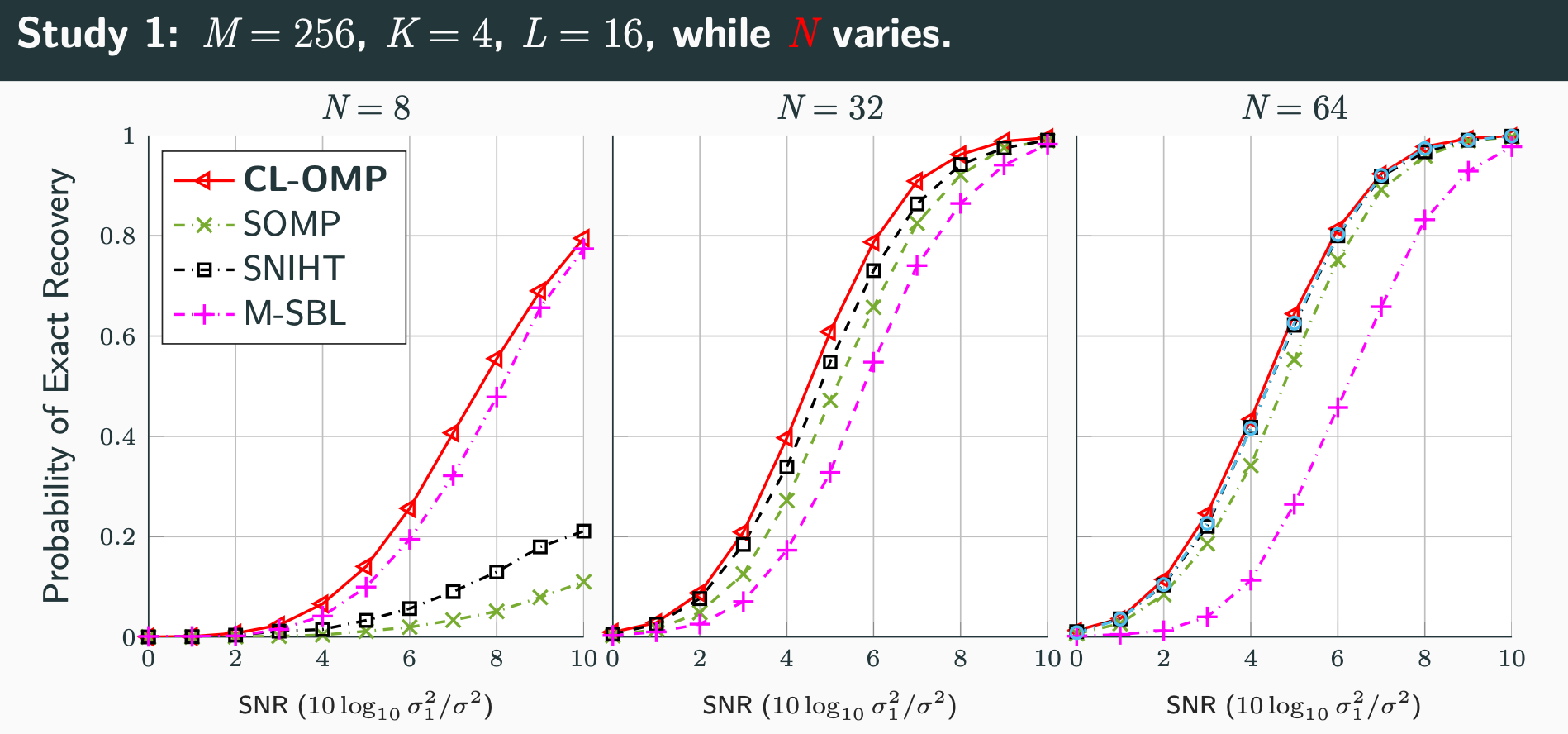

Covariance Learning Orthogonal Matching Pursuit (CL-OMP)

Code (both MATLAB and python functions) for the Covariance Learning Orthogonal Matching Pursuit (CL-OMP) method. Also a demo simulation that reproduces Figure 1 in the paper is provided.

Comparison in the simulation study is also made to SOMP, and a function to compute it is also provided.

For more information, see:

Matching Pursuit Covariance Learning, Esa Ollila Proc. 32nd European Signal Processing Conference (EUSIPCO'24), Lyon, August 26-30, 2024, pp. 2447-2451.

For more information, see:

Matching Pursuit Covariance Learning, Esa Ollila Proc. 32nd European Signal Processing Conference (EUSIPCO'24), Lyon, August 26-30, 2024, pp. 2447-2451.

[Github] [PDF] [Slides]

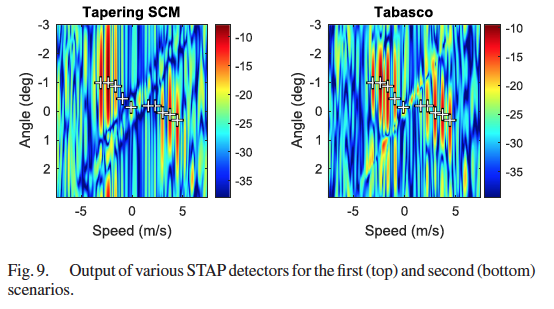

Regularized tapered sample covariance matrix

Tabasco toolbox provfilides an easy to use function for computing the TABASCO (TApered or BAnded Shrinkage COvariance) estimator.

Tabasco is a covariance matrix estimation method that combines tapering or banding of the sample covariance matrix with shrinkage towards scaled identity matrix. It enjoyes benefits of both approaches:

tapering/banding leverages on the assumed structure of the covariance matrix while optimal shrinkage guarantees that the obtained ovariance matrix estimator is positive definite,

while still preserving the structure applied using banding or tapering template. Optimal parameters, e.g., the bandwidth of banding matrix, or the shinkage intensity coefficient minimizing the MSE

are adaptively estimated from the data. We also include a demo example that reproduces Figure 2 (upper left corner plot) in our paper.

For more information, see:

Regularized Tapered Sample Covariance Matrix, Esa Ollila and Arnaud Breloy, IEEE Transactions on Signal Processing, vol. 70, pp. 2306-2320, 2022.

For more information, see:

Regularized Tapered Sample Covariance Matrix, Esa Ollila and Arnaud Breloy, IEEE Transactions on Signal Processing, vol. 70, pp. 2306-2320, 2022.

[Matlab toolbox]

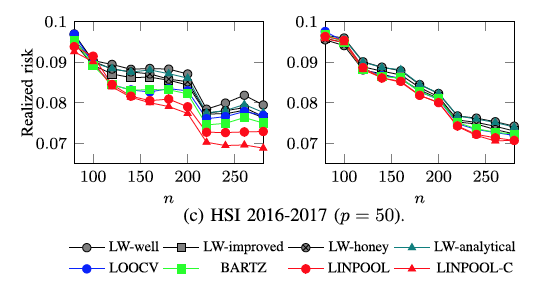

Linear pooling of sample covariance matrices

Linpool toolbox provides an easy to use function for computing an estimator of the population covariance matrix in the setting where there are data from K populations available.

We propose estimating each class covariance matrix as a distinct linear combination of all class sample covariance matrices. This approach is shown to reduce the estimation error when the sample sizes are limited, and the true class covariance matrices share a somewhat similar structure.

We provide an effective data adaptive method for computing the optimal coefficients in the linear combination that minimize the mean squared error under the general assumption that the samples are drawn from (unspecified) elliptically symmetric distributions.

An application in global minimum variance portfolio optimization using real stock data is also given.

For more information, see:

Linear Pooling of Sample Covariance Matrices, Elias Raninen, David E. Tyler, and Esa Ollila,IEEE Transactions on Signal Processing, vol. 70, pp. 659-672, 2022.

For more information, see:

Linear Pooling of Sample Covariance Matrices, Elias Raninen, David E. Tyler, and Esa Ollila,IEEE Transactions on Signal Processing, vol. 70, pp. 659-672, 2022.

[Matlab toolbox]

[ Slides]

[youtube video]

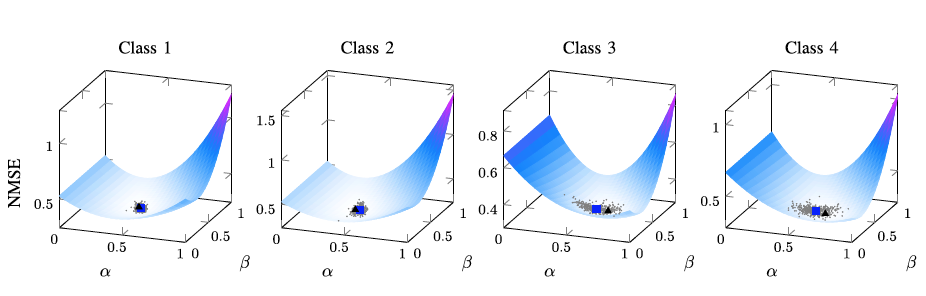

Coupled regularized sample covariance matrix estimator for multiple classes

CoupledRSCM toolbox for Matlab/R/python provides an easy to use function for computing regularized SCM (RSCM) estimators for multiclass problems that couple together two different target matrices for regularization: the pooled (average) SCM of the classes and the scaled identity matrix.

Regularization toward the pooled SCM is beneficial when the population covariances are similar, whereas regularization toward the identity matrix guarantees that the estimators are positive definite. We derive the MSE optimal tuning parameters for the estimators as well as propose a method for their estimation, avoiding commonly used computer intensive cross-validation.

For more information, see:

Coupled Regularized Sample Covariance Matrix

Estimator for Multiple Classes, Elias Raninen, David E. Tyler, and Esa Ollila,IEEE Transactions on Signal Processing, vol. 69, pp. 5681-5692, 2021

For more information, see:

Coupled Regularized Sample Covariance Matrix

Estimator for Multiple Classes, Elias Raninen, David E. Tyler, and Esa Ollila,IEEE Transactions on Signal Processing, vol. 69, pp. 5681-5692, 2021

[toolbox]

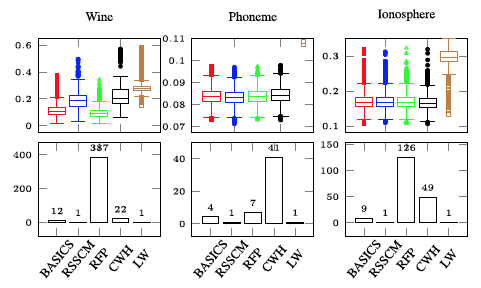

Bias adjusted sign covariance matrix

BASIC toolbox for Matlab provides an easy to use function for computing

the BASIC (Bias Adjusted SIgn Covariance) estimator as well as BASIC

Shrinkage estimator (BASICS), which is better suited for high

dimensional problems, where the dimension can be larger than the sample

size. It is well-known that the widely popular spatial sign covariance matrix (SSCM)

does not provide consistent estimates of the eigenvalues of the shape matrix (trace normalized covariance matrix).

BASIC alleviates this problem by performing an approximate bias correction to the eigenvalues of the SSCM.

For more information, see:

Bias adjusted sign covariance matrix, Elias Raninen and Esa Ollila,IEEE Signal Processing Letters, vol. 28, pp. 2092-2096, 2021.

For more information, see:

Bias adjusted sign covariance matrix, Elias Raninen and Esa Ollila,IEEE Signal Processing Letters, vol. 28, pp. 2092-2096, 2021.

[toolbox]

Shrinking the eigenvalues of M-estimators of covariance

shrinkM MATLAB toolbox is a collection of functions to compute an

M-estimator of scatter (covariance) matrix whose eigenvalues are shrinked

optimally towards the grand mean of the eigenvalues. Optimality means that

the shrinkage parameter is chosen to minimize the mean squared error

data-adaptively without computationally prohibitive cross-validation

procedure. The aforementioned shrinkage (or regularized) M-estimators of

covariance are described in detail in reference below. We also include a

demo example of using these covariance matrix estimators on

simulated data.

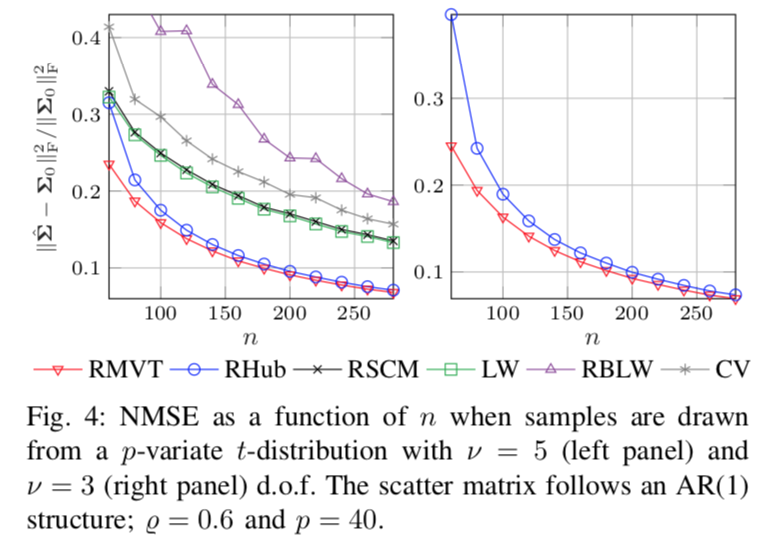

As can be noted, the proposed robust shrinkage M-estimators

(RMVT and RHub) outperform conventional non-robust estimators

with a large margin when data is non-Gaussian:

For more information, see

Shrinking the

eigenvalues of M-estimators of covariance matrix, Esa Ollila, Daniel P. Palomar and

Frederic Pascal, IEEE Transactions on Signal Processing, vol. 69, pp. 256-269, 2021.

For more information, see

Shrinking the

eigenvalues of M-estimators of covariance matrix, Esa Ollila, Daniel P. Palomar and

Frederic Pascal, IEEE Transactions on Signal Processing, vol. 69, pp. 256-269, 2021.

[Matlab toolbox]

[ Slides]

[youtube video]

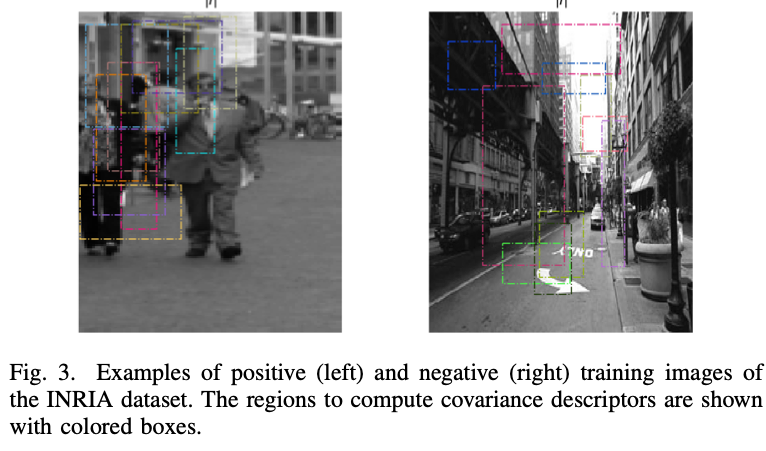

Pedestrian detection using Riemannian classification algorithms

We have developed a python toolbox for pedestrian detection from images using classification algorithms that utilize Riemannian geometry.

For more information, see

A Comparative Study of Supervised Learning Algorithms for Symmetric Positive Definite Features, Ammar Mian, Elias Raninen and Esa Ollila,

Proc. European Signal Processing Conference (EUSIPCO'20), Amsterdam, Netherlands, August 24-28, pp. 950-954. 2020.

For more information, see

A Comparative Study of Supervised Learning Algorithms for Symmetric Positive Definite Features, Ammar Mian, Elias Raninen and Esa Ollila,

Proc. European Signal Processing Conference (EUSIPCO'20), Amsterdam, Netherlands, August 24-28, pp. 950-954. 2020.

[ Python toolbox]

[pdf]

Python toolbox]

[pdf]

Block-wise Minimization-Majorization algorithm for Huber's criterion

Huber's criterion can be used for robust joint estimation of regression and scale parameters in the linear model.

The codes use the block-wise minimization majorization framework with novel data-adaptive

step sizes proposed in our paper for both the location and scale. Sparse signal

recovery using Huber's criterion can be performed using the normalized iterative

hard thresholding approach which is also implemented in the toolbox. We

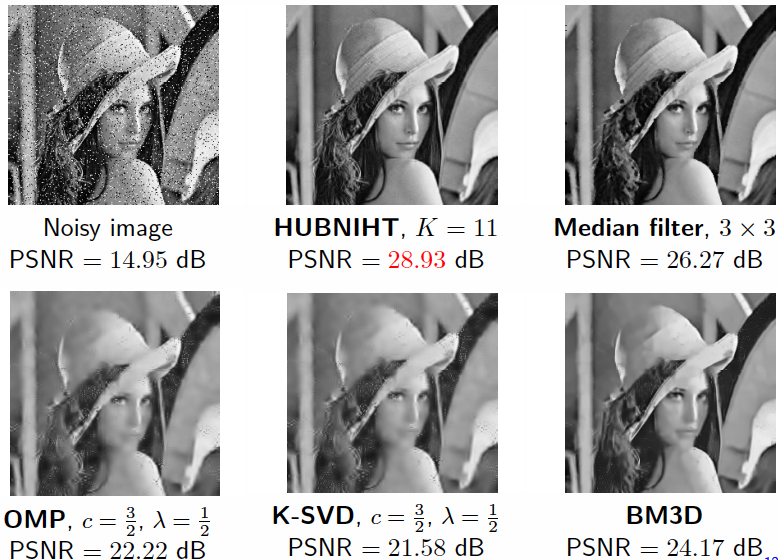

illustrate the usefulness of the algorithms, hubreg and hubniht

in an image denoising application and simulation studies. For image denoising,

we provide an easy-to-use function hubniht_denoising. An example of HUBNIHT denoising

performance of Lena image in salt-and-peper noise is shown below:

and the Matlab script that produced the results is shown here.

and the Matlab script that produced the results is shown here.

For more information about the method, see

Block-wise minimization-majorization algorithm for Huber's criterion:

sparse learning and applications by Esa Ollila and Ammar Mian, in

Proc. IEEE International Workshop on Machine Learning for Signal Processing (MLSP'20),

Sep 21-24, 2020, Espoo, Finland, pp. 1-6.

[Toolbox]

[Slides]

Compressive Regularized Discriminant Analysis

CompressiveRDA MATLAB toolbox contains function to compute the CRDA classifiers

introduced in the reference below. The proposed classifiers can be applied in

high-dimensional sparse data scenarios, where the sample size is smaller than

the dimension of the data, which is potentially very large. Our method is especially designed for feature selection purposes and can be used as a gene selection method in genomic studies. The toolbox also contains demo examples of classification

of real-world data sets used in our paper.

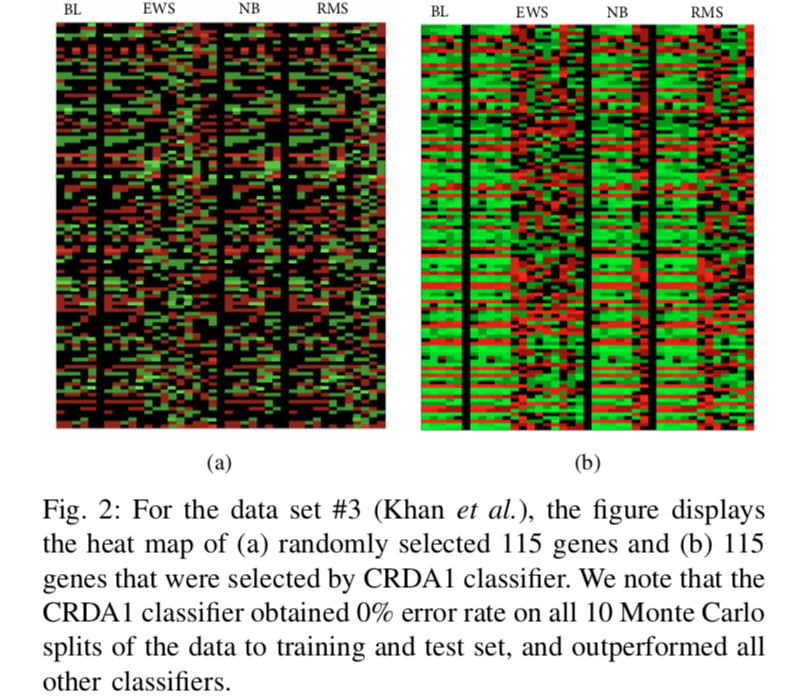

One reason for success of CRDA can be its ability to find patterns in data as

shown in this gene heat map:

For more information, see

A Compressive Classification Framework for High-Dimensional Data,

Muhammad N. Tabassum and Esa Ollila, IEEE Open Journal of Signal Processing, Vol 1., pp. 177-186, 2020.

For more information, see

A Compressive Classification Framework for High-Dimensional Data,

Muhammad N. Tabassum and Esa Ollila, IEEE Open Journal of Signal Processing, Vol 1., pp. 177-186, 2020.

[Matlab toolbox]

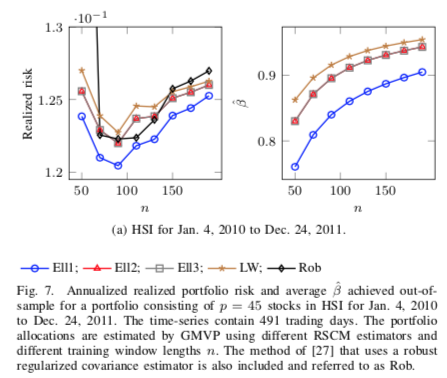

Regularized Sample Covariance Matrix (RSCM) Estimator

RegularizedSCM MATLAB toolbox contains function to compute the Ell-RSCM estimators of the

covariance matrix introduced in the reference below. The proposed estimators can be applied in

high-dimensional sparse data scenarios, where the sample size is smaller than

the dimension of the data, which is potentially very large.

The toolbox also contains demo examples arising from finance and classification.

In the former, the estimators are applied in portfolio

optimization problem of real data, where we use historical (daily) stock

returns from the Hong Kong's Hang Seng Index (HSI) and

Standard and Poor's 500 (S&P 500) index. In the latter, the estimators are used

in classification problem of real data sets using the framework of regularized

discriminant analysis. In both cases, the proposed estimators are able to yield better

performance than the state-of-the-art methods. See example below:

For more information, see

Optimal shrinkage covariance

matrix estimation under random sampling from elliptical distributions,

Esa Ollila and Elias Raninen, IEEE Transactions on Signal Processing, vol. 67, no. 10, pp. 2707 - 2719, 2019.

For more information, see

Optimal shrinkage covariance

matrix estimation under random sampling from elliptical distributions,

Esa Ollila and Elias Raninen, IEEE Transactions on Signal Processing, vol. 67, no. 10, pp. 2707 - 2719, 2019.

[Matlab toolbox]

[ Slides]

[youtube video]

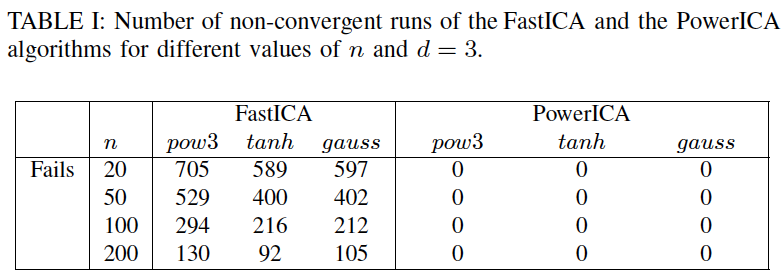

Novel FastICA power iteration algorithm

This MATLAB toolbox contains function to compute the fastICA power iteration estimator,

called PowerICA, that was proposed in the reference below. PowerICA method is efficient

alternative to conventional FastICA estimator in the cases when the sample size is not orders

of magnitude larger than the data dimensionality. This is the finite-sample regime in which

the (fixed-point) FastICA algorithm is often reported to have convergence problems. The

estimator is thus useful in many real data problems where FastICA is commonly used

such as blind-source separation of fMRI data. This is illustrated in the simulation example below:

For more information, see

Alternative derivation of FastICA with novel power iteration algorithm,

Shahab Basiri, Esa Ollila and Visa Koivunen, IEEE Signal Processing Letters, vol. 24, no 9, 2017.

For more information, see

Alternative derivation of FastICA with novel power iteration algorithm,

Shahab Basiri, Esa Ollila and Visa Koivunen, IEEE Signal Processing Letters, vol. 24, no 9, 2017.

[Matlab toolbox]

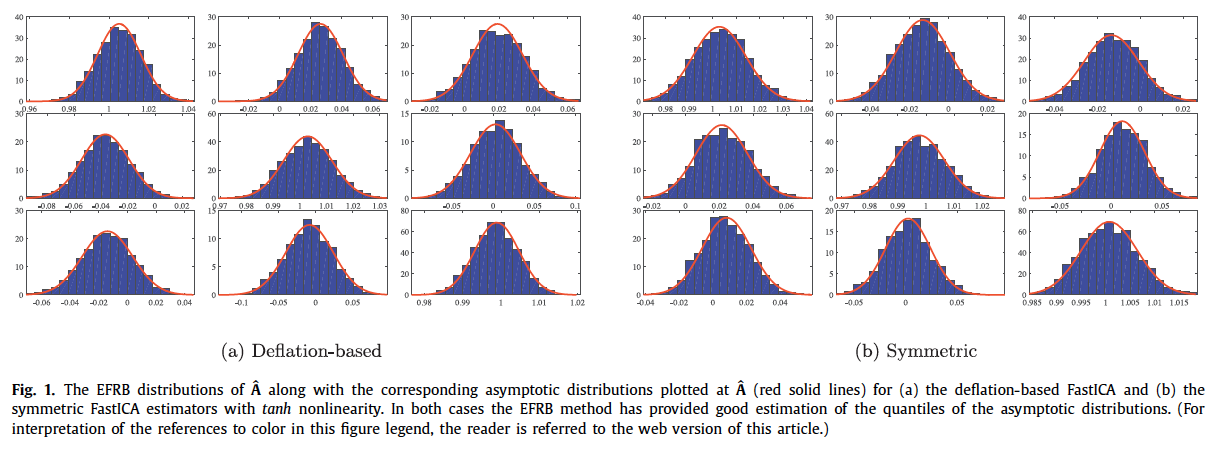

Reliable and fast bootstrap-based inference in the ICA model

This software contains function to compute the low complexity and stable bootstrap procedure

for FastICA estimators, referred to as enhanced fast and robust bootstrap (EFRB) method

for FastICA, which was introduced in the reference below.

Our bootstrapping techniques allow for performing cost efficient and reliable

bootstrap-based statistical inference in the ICA model. Performing statistical

inference is needed to quantitatively assess the quality of the estimators and

testing hypotheses on mixing coefficients in the ICA model. EFRB is shown to provice

accurate description of the distribution of FastICA mixing matrix estimator:

For more information, see

Enhanced bootstrap method for statistical inference in the ICA model

For more information, see

Enhanced bootstrap method for statistical inference in the ICA model

Shahab Basiri, Esa Ollila and Visa Koivunen, Signal Processing, vol. 138, pp. 53-62, 2017

[Matlab code]

Sparse signal recovery in the multiple measurements vector model

Download the MATLAB function that computes the HUB-SNIHT estimator introduced in the reference below.

The estimator solves the multichannel sparse recovery problem of complex-valued measurements

where the objective is to find good recovery of jointly sparse unknown signal vectors from

the given multiple measurement vectors which are different linear combinations of the same

known elementary basis vectors or dictionary.

For more information, see

Multichannel sparse recovery of complex-valued signals using Huber's criterion

Esa Ollila, in Proc. Int'l Workshop on Compressed Sensing Theory and its Applications to Radar, Sonar and Remote Sensing (CoSeRa'15), Pisa, Italy, June 16-19, 2015, pp. 32-36.

[Matlab code]

Tests of circularity

Software to compute the tests of circularity introduced in Adjusting the generalized likelihood

ratio test of circularity robust to non-normality, Esa Ollila and Visa Koivunen,

in Proc. 10th IEEE Int.'l Workshop on Signal Processing Advances in Wireless Communications

(SPAWC'09), Perugia, Italy, June 21-24, 2009, pp. 558 - 562.

[Matlab code]

Also includes code for GLRT of circularity introduced in Generalized complex elliptical distributions

Tools for (non-circular) complex elliptically symmetric distributions

This software package contains a collection of tools for random number generation from

complex elliptically symmetric (CES) distributions (including

complex normal (Gaussian), complex t-, complex generalized Gaussian, (isotropic) symmetric alpha-stable distribution)

and Wald's type circularity test.

For more information, see

Complex elliptically symmetric random

variables - generation, characterization and circularity tests,

Esa Ollila, Jan Eriksson and Visa Koivunen, IEEE Transactions on signal processing, vol. 59, no.1, pp. 58-69, 2011.

[Matlab code]

Robust regression based on Oja ranks

Software to compute the regression coefficent estimates based on Oja ranks introduced in

Estimates of regression coefficients based on lift rank covariance matrix,

Esa Ollila, Hannu Oja and Visa Koivunen, Journal of the American Statistical Association, vol. 98, no. 461, pp. 90-98, 2003.

[C code and R code]